MIAMI REAL ESTATE OVERVIEW: 5-YEAR TRENDS AND CURRENT DYNAMICS

Within the dynamic realm of Miami’s real estate, three key sectors stand prominent: the thriving office market, the fluctuating yet resilient retail landscape, and the evolving multifamily housing sector. These sectors encapsulate the energy of Miami’s real estate scene, where shifts in demand, supply, and economic influences intertwine to shape the city’s property dynamics.

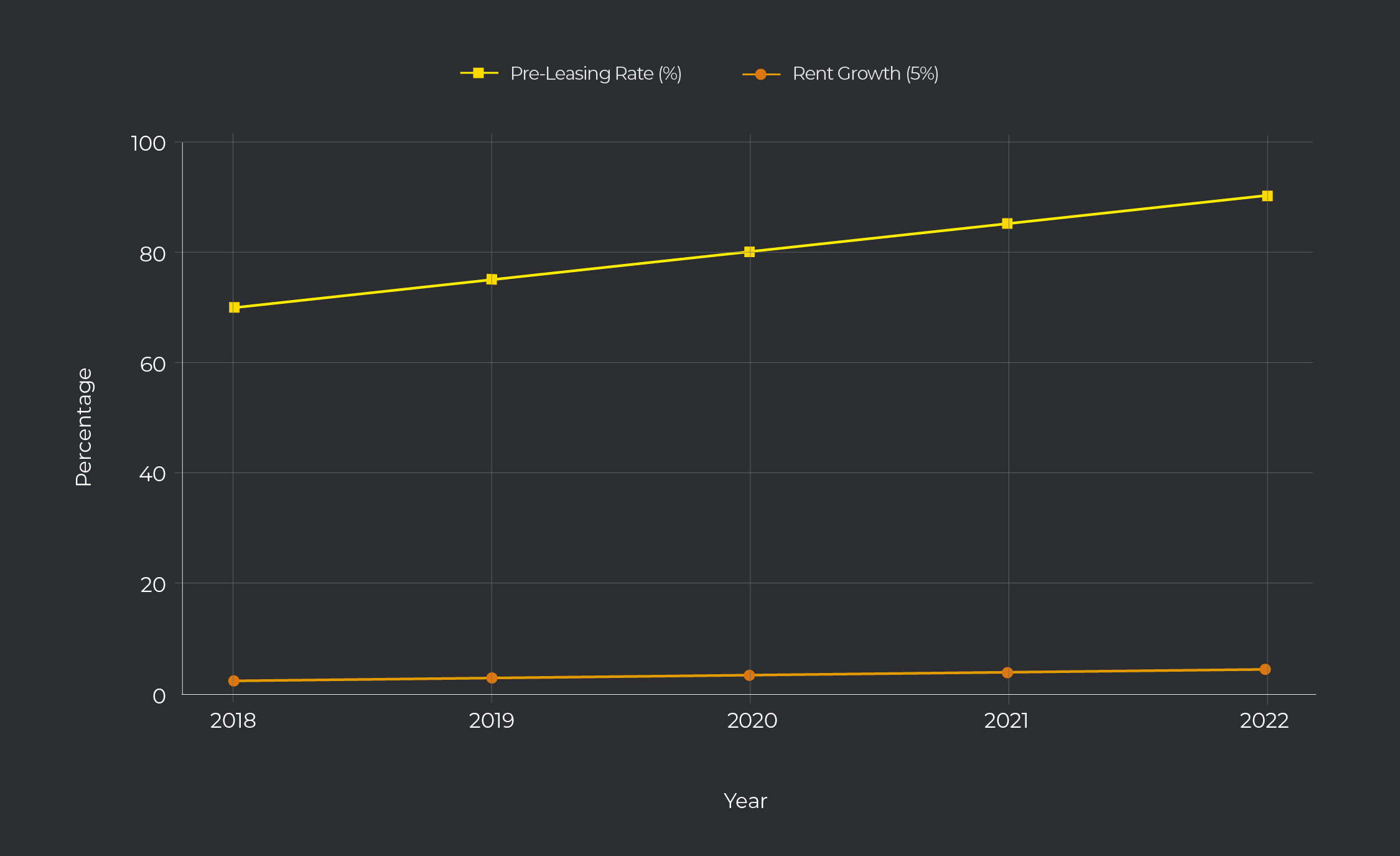

OFFICE MARKET SUMMARY

Miami’s office market is flourishing post-pandemic, with demand for downtown space outstripping supply, leading to rent growth. The city’s appeal, coupled with a scarcity of high-quality spaces, is expected to keep rent increases ahead of the national trend. Construction is vigorous, but the pre-leasing of new spaces shows a strong market demand. Despite a national downtrend, Miami’s office values have risen, and investor activity remains buoyant, signifying confidence in the market’s resilience.

HIGHLIGHTS & KPI’S:

Demand: High demand in downtown areas.

Rent Growth: Rent increases likely to surpass the national average.

Construction: Active, with new spaces mostly pre-leased.

Investor Activity: Remains strong despite a slowdown.

Rates: High pre-leasing rates indicating robust demand.

Office Market KPI's

Rent Growth over the years in percentage.

Pre-Leasing Rate as a percentage, indicating the rate at which new office spaces are being leased before completion.

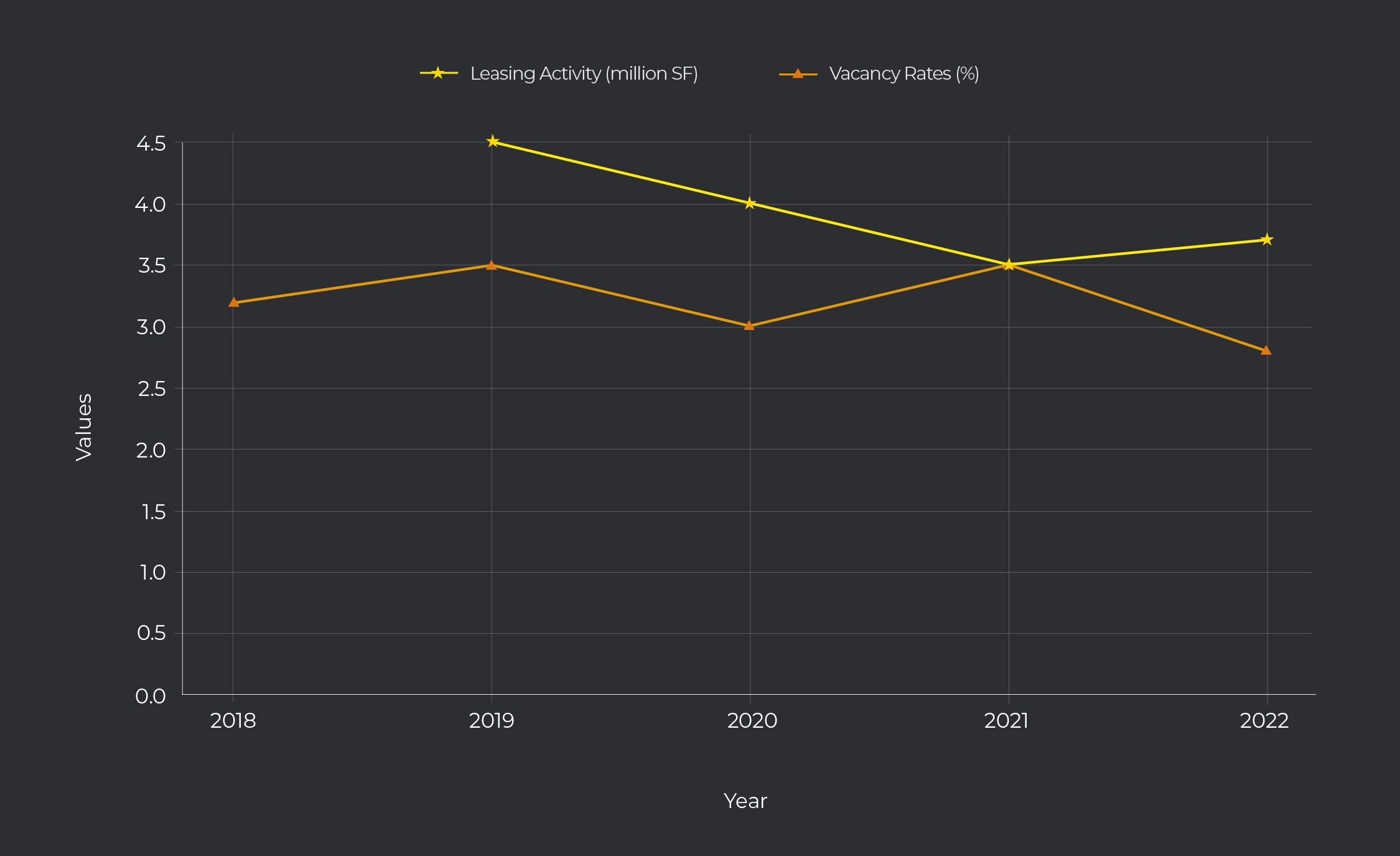

RETAIL MARKET SUMMARY

Despite a downturn in leasing activity, Miami’s retail market maintains low vacancy rates due to continued positive net absorption. The market is underpinned by strong fundamentals, including income growth and a rebound in tourism, which support consumer spending. While new construction is concentrated in key areas, growth has moderated, and the retail landscape remains stable with tight availability.

HIGHLIGHTS & KPI’S:

Consumer spending: Continues to underpin the retail market despite economic headwinds.

Leasing Activity: 2.8 million SF leased by Q3 2023, down from peak. Leasing activity has decreased, but the market remains tight.

Vacancy Rates: Maintained at a low 3.7%, with positive net absorption keeping availability rates low.

Retail Market KPI's

Leasing Activity measured in millions of square feet over the years.

Vacancy Rates in percentage, showing the proportion of all available retail spaces that are not leased.

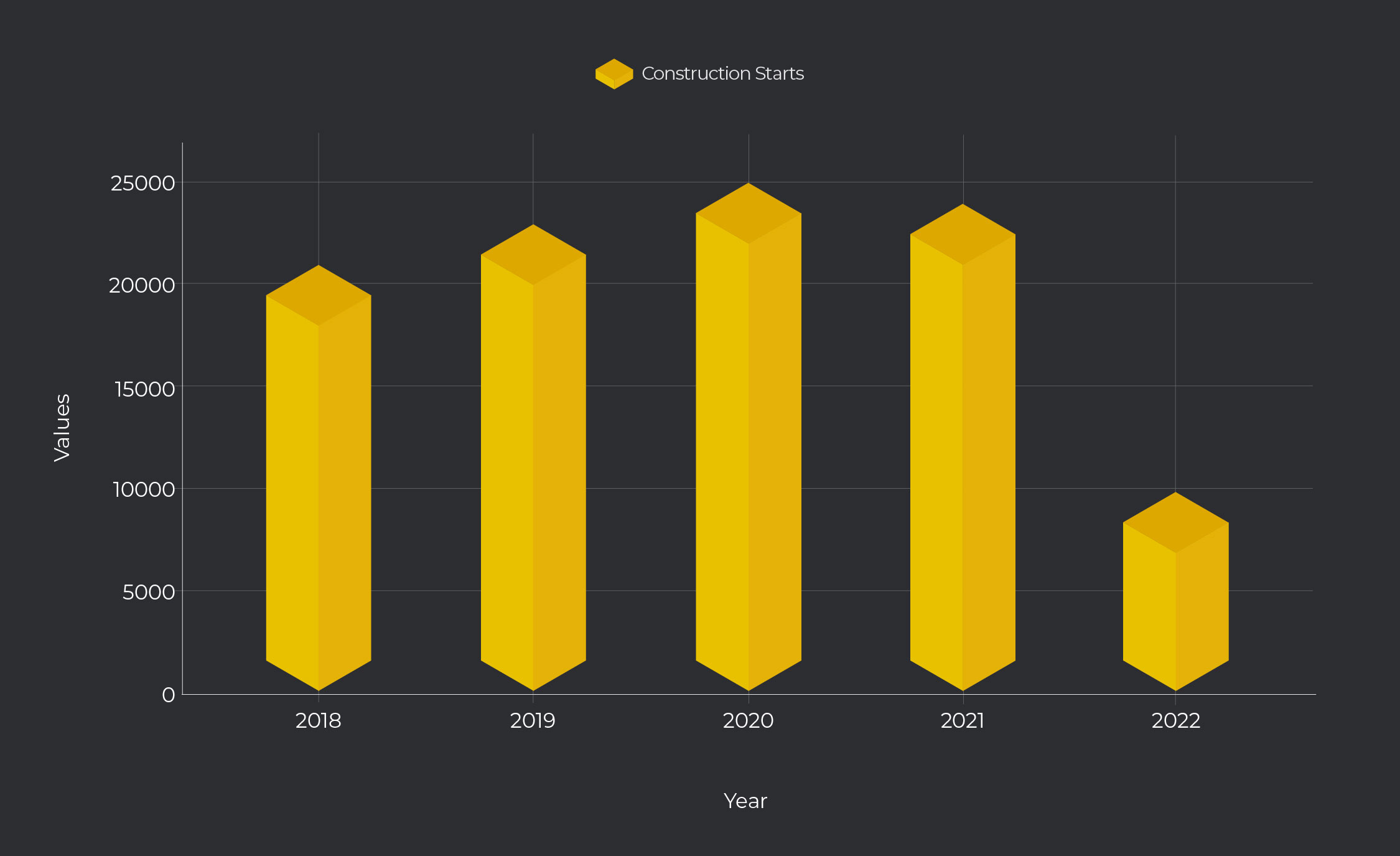

MULTIFAMILY HOUSING SECTOR SUMMARY

The multifamily market in Miami shows a cooling trend, with a decrease in demand and slowing rent growth. However, the vacancy rate remains below the national average, and the sector is expected to benefit from the economic recovery, especially in the affordable housing segment. Despite fewer construction starts, a significant number of new units are still anticipated to be delivered, maintaining a healthy supply in the housing market.

HIGHLIGHTS & KPI’S:

New Constructions: Construction has slowed, with future deliveries expected to sustain market supply.

Construction: Dropped to 6,800 units in 2023 after a peak in 2022.

Sales Volume: $1.4 billion, slightly below the five-year average.

Multifamily Housing Market KPI's

Vacancy Rate in percentage, indicating the proportion of all available multifamily units that are not leased.

Rent Growth year over year in percentage.

Construction showing the number of new multifamily units that began construction.

*The information and insights in this market summary were obtained from CoStar Group. With their comprehensive data and analytical expertise, CoStar Group remains a pivotal source, enabling a deeper understanding of the real estate landscape. This article draws upon their expertise to present an overview of trends and developments within the industry in Miami.